ARCH models

Auto-Regressive Conditional Heteroskedasticity (ARCH) models

|

|

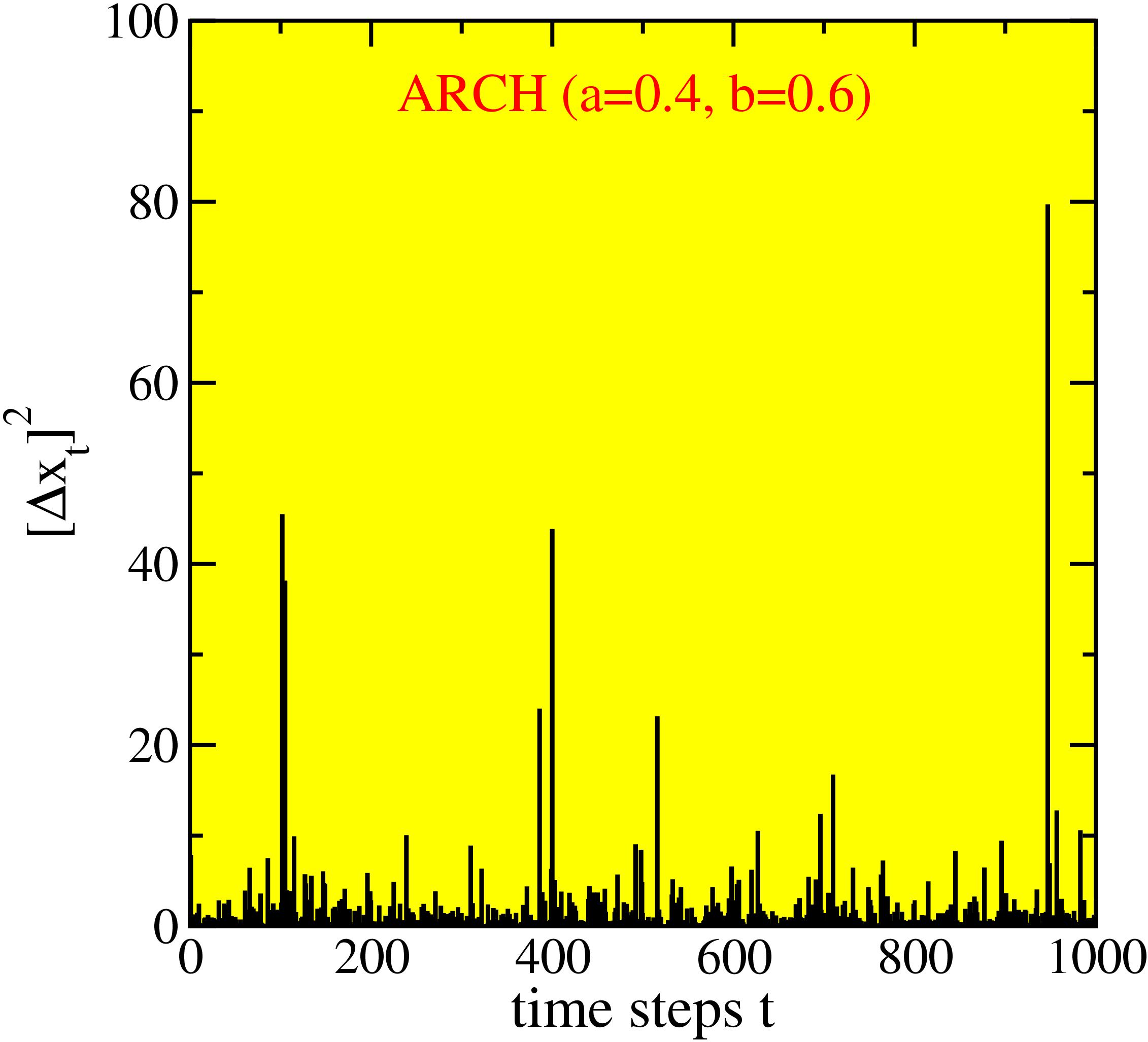

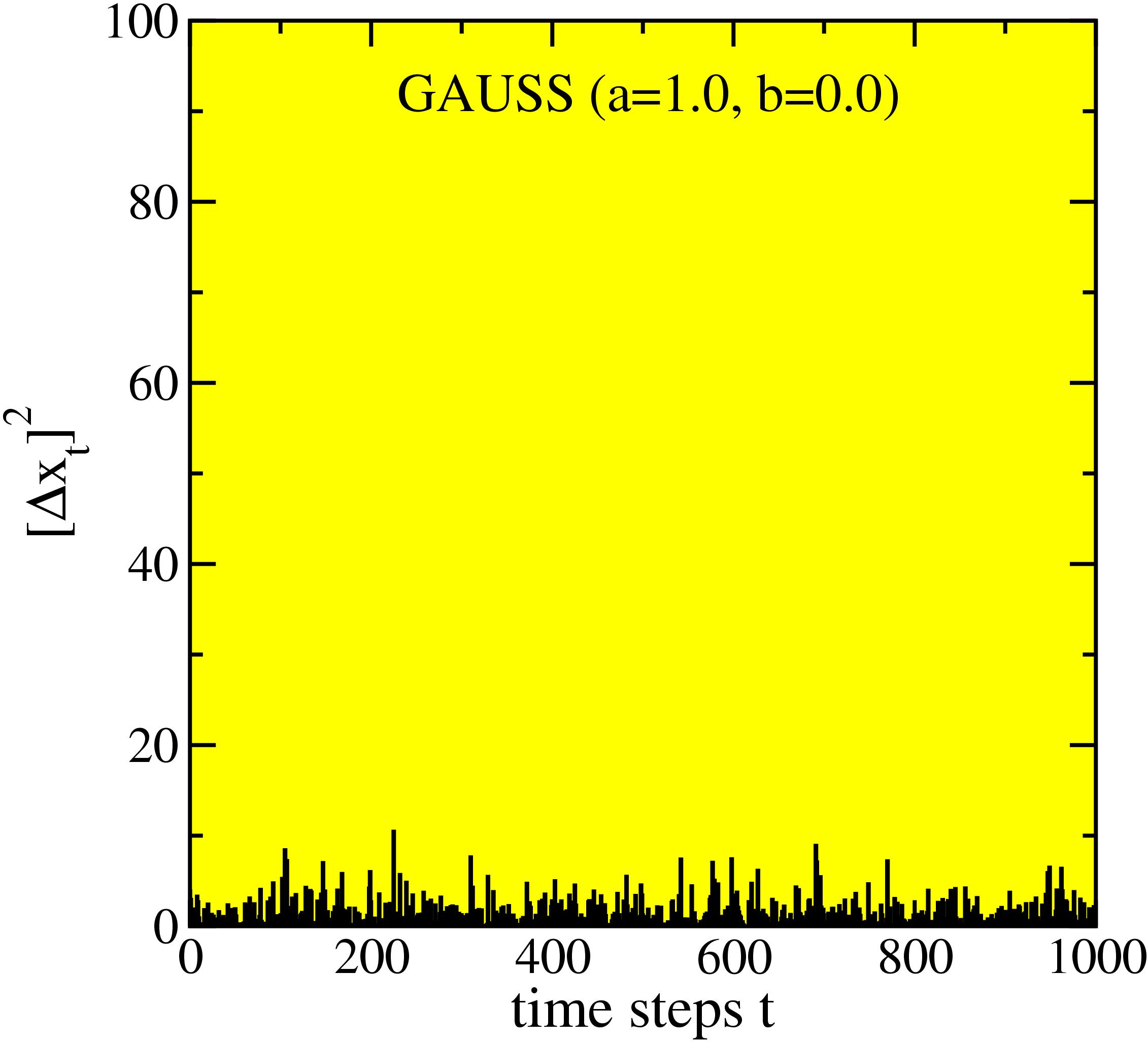

The left panel shows a sequence of the square of an ARCH

variable versus time steps, for the case of mean unit variance. The right panel displays a sequence of

the square of a Gaussian variable of unit variance. The probability distribution function of the ARCH

variable has power-law tails (see e.g.

[P79]).